Page 268 - DSD ANNUAL REPORT 2022-2

P. 268

P AR T E: FINANCIAL INFORMA TION SOCIAL RELIEF FUND

PART E: FINANCIAL INFORMATION

Notes to the Financial Statements of the Social Relief Fund for the year Notes to the Financial Statements of the Social Relief Fund for the year Y ear

ements

The

o

The Financial Stat

Of

e R

elief Fund For

The R

efuge

Not

Notes To The Financial Statements Of The Refugee Relief Fund For The Year

T

es

ended 31 March 2022 ended 31 March 2022

Ended 31 March 2022

Ended 31 March 2022

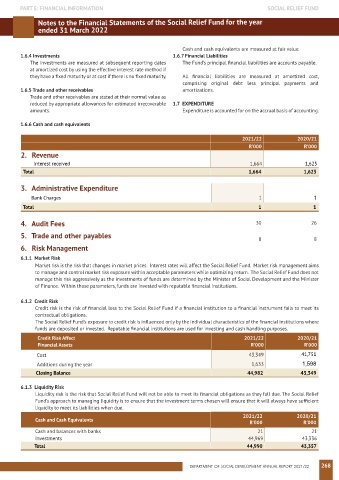

Cash and cash equivalents are measured at fair value.

1.6.4 Investments 1.6.7 Financial Liabilities

The investments are measured at subsequent reporting dates The Fund’s principal financial liabilities are accounts payable.

at amortized cost by using the effective interest rate method if

they have a fixed maturity or at cost if there is no fixed maturity. All financial liabilities are measured at amortized cost,

comprising original debt less principal payments and

1.6.5 Trade and other receivables amortizations.

Trade and other receivables are stated at their normal value as

reduced by appropriate allowances for estimated irrecoverable 1.7 EXPENDITURE

amounts. Expenditure is accounted for on the accrual basis of accounting.

1.6.6 Cash and cash equivalents

2021/22 2020/21

R’000 R’000

2. Revenue

Interest received 1,664 1,625

Total 1,664 1,625

3. Administrative Expenditure

Bank Charges 1 1

Total 1 1

4. Audit Fees 30 26

5. Trade and other payables 8 8

6. Risk Management

6.1.1 Market Risk

Market risk is the risk that changes in market prices. Interest rates will affect the Social Relief Fund. Market risk management aims

to manage and control market risk exposure within acceptable parameters while optimizing return. The Social Relief Fund does not

manage this risk aggressively as the investments of funds are determined by the Minister of Social Development and the Minister

of Finance. Within these parameters, funds are invested with reputable financial institutions.

6.1.2 Credit Risk

Credit risk is the risk of financial loss to the Social Relief Fund if a financial institution to a financial instrument fails to meet its

contractual obligations.

The Social Relief Fund’s exposure to credit risk is influenced only by the individual characteristics of the financial institutions where

funds are deposited or invested. Reputable financial institutions are used for investing and cash handling purposes.

Credit Risk Affect 2021/22 2020/21

Financial Assets R’000 R’000

Cost 43,349 41,751

Additions during the year 1,633 1,598

Closing Balance 44,982 43,349

6.1.3 Liquidity Risk

Liquidity risk is the risk that Social Relief Fund will not be able to meet its financial obligations as they fall due. The Social Relief

Fund’s approach to managing liquidity is to ensure that the investment terms chosen will ensure that it will always have sufficient

liquidity to meet its liabilities when due.

2021/22 2020/21

Cash and Cash Equivalents

R’000 R’000

Cash and balances with banks 21 21

Investments 44,969 43,336

Total 44,990 43,357

DEPARTMENT OF SOCIAL DEVELOPMENT ANNUAL REPORT 2021/22 268